Hospital insurance riders in Singapore can feel like a maze of co-payment percentages and panel restrictions — here’s a plain-language walkthrough.

IMPORTANT : This is particularly relevant to those who have a private hospitalisation plan AND

– have an option C rider under Aviva Myshield (regardless of when it was purchased) OR

– purchased full cover IP (Integrated Shield Plan) riders with any insurer on or after 8 Mar’18.

As you are probably aware, all the IP insurers have made changes to their plans in line with the MOH announcement back in Mar’18, requiring co-payment features for IP riders by 1 April 2019.

With the exception of Aviva, for those who bought IP riders before 8 Mar’18, you will continue to enjoy your rider with benefits unchanged. For Aviva policyholders, pls see “New Aviva Option C rider” below.

For those who bought full cover IP riders between March 8 last year to March 31 this year, your plan will transition to the new co-pay riders upon the renewal of your policies from April 1, 2021.

NEW Co-pay riders (how it works in general)

So how does the new co-pay riders look? Depending on which insurer and plan (we will assume private hospitalisation for discussion purpose) you are with, it may have the following features :-

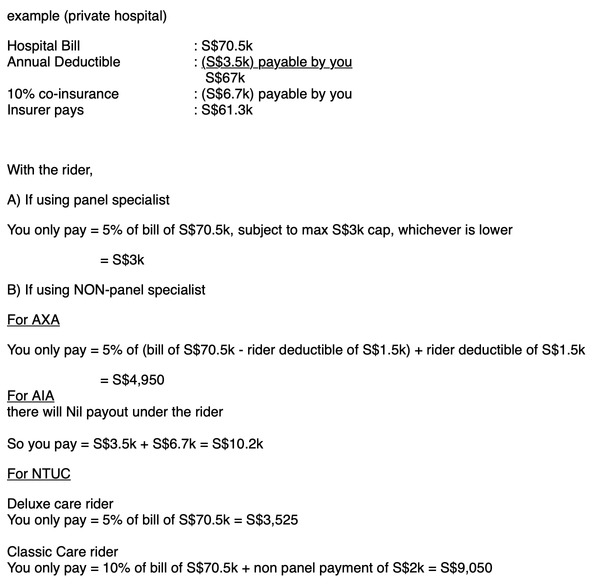

1. 5% co-payment by you subject to a cap of S$3k/yr if you are using the insurer’s panel of specialists. No cap if using non-panel

2. AXA, Aviva and NTUC require an additional rider deductible to be payable by you if using non-panel specialist

3. AIA rider will not cover main plan deductible and co-insurance at all if using non-panel specialist

This is applicable if you bought the option C (combination of

– there is now a rider deductible payable by you as highlighted in the table below (Existing MyHealthPlus column)

– amount of rider deductible is dependent on whether panel specialist is used &/or pre-authorisation is given. Please refer to the

New Aviva Option C rider (pls refer to Existing MyHealthPlus column in the table below)

New Aviva Option C II rider

This is applicable if you bought the option C (combination of

Essentially, the Option C II rider covers

– the main plan deductible after you pay a rider deductible (pls refer to

– 50% of the main plan co-insurance (your exposure is cap at S$3k if using panel specialist with pre-authorisation, otherwise no cap)

Insurer panel of specialists and pre-authorisation

In practice, on the issue of using the insurer’s panel of specialists and pre-authorisation, there may be a tendency for policyholders to overlook this as the specialist they see will often be referred by their GP or referred by their friends. Hence, there’s a possibility that your preferred specialist may not fall under the insurer’s panel.

This concern is real as I’m usually informed by my clients on their impending hospitalisation or surgery just days before the surgery or hospitalisation.

Moving forward, pls use the insurer’s panel of specialist (click on the link)

Aviva_MyHealthPlus_MyShield_BrochureDownload

AXA panel of specialists

AXA shield

AIA panel of specialists

AIA Healthshield Gold Max

To meet up for a discussion, just hit reply and we’ll get in touch soon.